Investing is all about benchmarks. If you’re a passive investor, tracking the right benchmark index is critical to getting the kind of returns you want. If you’re an active manager, picking the right index to benchmark your success is important to gathering assets and providing investors with the right portfolio tools. Picking the best benchmark is vital in all forms of investing.

Unfortunately, when it comes to fixed income investing, we may all be choosing the wrong benchmark to follow.

Billions of dollars’ worth of investor assets—both big and small—is linked to the Bloomberg Barclays Aggregate Bond Index or Agg. This includes both actively managed funds benchmarked to the index as well as passive investments actually tracking the bonds held within it. And yet, the Agg may not be the best way to gauge our fixed income success going forward. New research suggests that it’s time to rethink how we look at our fixed income portfolios.

Don’t forget to check our Fixed Income Channel to learn more about generating income in the current market conditions.

A Quick Dive

Just like the S&P 500 and MSCI EAFE Index, the Bloomberg Barclays Aggregate Bond Index—sometimes referred to as the BarCap—has become the de-facto benchmark and index for fixed income investors. More than 90% of all investors use the Aggregate Bond Index as their benchmark. And it’s easy to see why. The index was created in 1986 and is designed to be representative of the entire investment-grade quality or better bond universe in the United States.

To be included, a security must have at least one year left to maturity, and have an outstanding par value of at least $100 million. This universe of bonds includes U.S. Treasuries, agency bonds, asset-backed securities, mortgage-backed securities, and corporate bonds. Munis and inflation-protected securities are excluded due to their tax differences. As of its last rebalance in April 2021, the index included more than 9,500 different bonds among its mix.

Given its size and scope, it’s understandable how and why the Agg has become the top index for benchmarking fixed income success. If you’re looking for steady-eddy bonds to balance out an equity portfolio, the mix of investments in the Agg should provide just what you’re looking for.

Or at least that’s the theory.

The BarCap’s Shortcomings

Despite being THE benchmark, the Agg has a lot of issues in its construction and underlying holdings. And some of these issues could become real problems down the road.

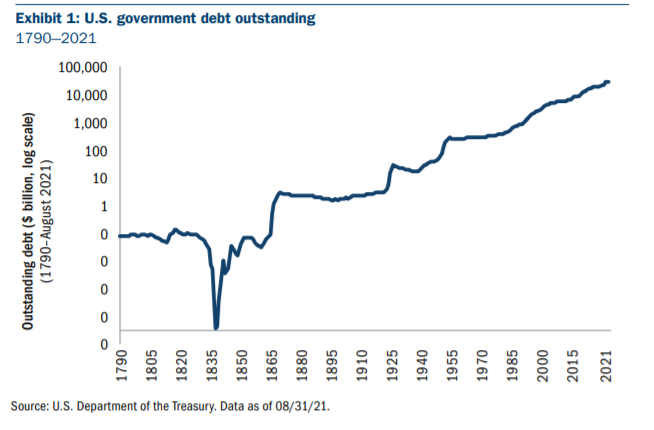

For starters, the index is market-cap weighted. In the stock world, market-cap weighted indexes aren’t necessarily a problem. But for fixed income, it can be. The reason is that market-cap based fixed income indexes are overweight based on the amount of debt outstanding. That is, the firms with the most debt get a higher place in the index. Essentially, you’re rewarding the biggest debtors with more pull on the index. In the case of the Agg, that’s the U.S. government.

You can see by this chart from Columbia Threadneedle just how much debt the U.S. government has taken on throughout its history.

Source: Columbia Threadneedle

Ignoring the political talking points about the U.S. debt, the effect on the Agg is profound. Columbia found that back in 2007, only about 22% of the Agg was in U.S. Treasuries. Today, that number is nearly 40%. All in all, more than two-thirds of all its holdings are now in government debt, specifically Treasuries and U.S. government-backed mortgage debt. The problem is that these two types of bonds have a nearly 81% correlation to each other. They basically move the same way. Despite having 9,500 bonds, the Agg doesn’t provide a lot of diversification benefits within fixed income.

Secondly, the Agg exposes investors to plenty of interest rate risk. When the benchmark was created, it was the 1980s and inflation was running super high. Since then, rates have continued to fall from these record levels and, thanks to the Great Recession/COVID-19 crisis, sit at zero. As a result, the Agg has never shown any losses. That’s about to change.

The average duration in the Agg is just under seven years. Duration is essentially how sensitive a bond’s price is relative to interest rates, both increases and decreases. As rates rise, bond prices fall as investors can buy new bonds with higher coupon payments. So, a bond with a duration of 2.5 years would see a 2.5% drop in price on a 1-percentage point increase in interest rates. In the case of the Agg, we’re looking at a 7% drop for each 1-percentage point increase in rates. Given the Fed’s stance and the rise in inflation, investors are essentially setting themselves up for losses sooner than later.

Finally, the yield on the Agg is well below historical norms. After a decade of near-zero rates, the Agg is currently yielding just 1.40%. That’s about half as much as ten years ago.

Be sure to check out our Portfolio Management Channel to learn more about building or rebalancing your portfolio.

Rethinking the Benchmark

Given the Agg’s shortcomings and issues, fixed income investors may want to rethink how they benchmark or track bonds in their portfolios.

For one thing, don’t put all of your eggs in one basket. Given the lack of diversification benefits in the Agg, investors may not want to use it as their only bond position. Corporates, junk bonds, munis, and other security types function and correlate differently than U.S. treasuries. And many other bond types can offer similar credit quality to government bonds. With their large cash balances, I would argue that a bond from Microsoft (MSFT) or Apple (AAPL) is just as good as one from the U.S. Treasury at this point.

Secondly, duration is a key factor, especially for those near or about to retire. While generating income is important, the high duration of the index means that investors will see losses sooner rather than later. This can be a major problem for those using their portfolios to live on in their golden years.

Finally, active management using a total return strategy could be best for younger investors looking to buy the best bonds at cheap prices. There’s plenty of evidence suggesting that fixed income is the best place for an active role.

In the end, the Bloomberg Barclays Aggregate Bond Index has served investors well. But now, it might be time to retire the Agg and rethink our bond allocations.

Be sure to check our News section to keep track on the latest news on the income investing front.